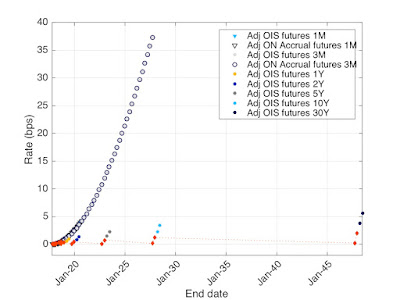

SOFR: multiple basis

A couple of weeks ago, CME announced that they cleared their first SOFR-linked swaps . The first trades where cleared by BNP Paribas, Credit Suisse, J.P. Morgan, Morgan Stanley and NatWest Markets. The total notional was USD 200 million without details on the type of swaps or their maturity. The main difference between the SOFR-linked swaps cleared at LCH and those cleared at CME is the Price Alignment Interest (PAI)/collateral rate. For LCH it is EFFR while for CME it is the SOFR itself. Both CCPs accept OIS (Fixed v SOFR) and basis (LIBOR v SOFR and EFFR v SOFR). Also LIBOR, EFFR and SOFR futures are traded. This means that now we have the full spectrum of legs types, PAI and adjustments: LIBOR leg with EFFR collateral (LCH, CME, bilateral) OIS-EFFR leg with EFFR collateral (LCH, CME, bilateral) OIS-SOFR leg with EFFR collateral (LCH, bilateral?) LIBOR leg with SOFR collateral (CME in basis swaps) OIS-EFFR leg with SOFR collateral (CME in basis swaps) OIS-SOFR leg w...