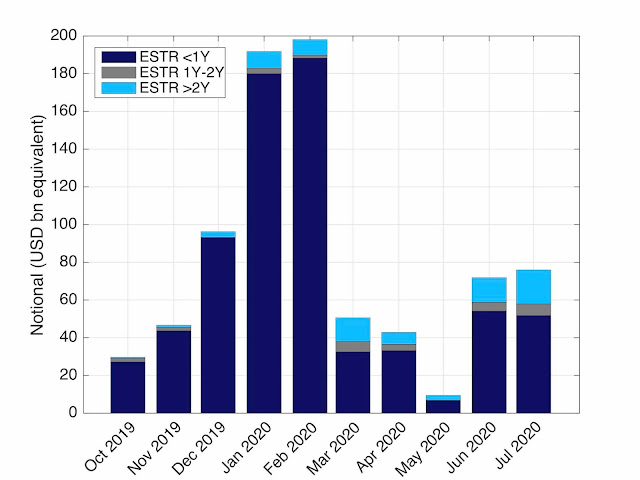

FRAs moving to SPSs

Market is moving out of Forward Rate Agreements (FRA) with FRA Discounting settlement method to Single Period Swaps (SPS). Some statistics about this market move can be found in a recent blog by Clarus: Toxic FRAs, Fallbacks and Single Period Swaps I'm glad to see that my warning from two years ago about the inadequacy for ISDA fallback for FRAs has made its way to an important market development. Early warning were published on this blog, in Consultation on IBOR fallbacks: Question 1 and later in quantitative finance on-line repositories and reported in the press in FRAs won’t work with standard Libor fallback, experts say . This development is coming in parallel with the push by CCPs to move to OIS directly instead of ISDA-designed fallback. That proposal has been reported recently in the press and commented in a previous blog: Wow! - LCH plans Libor swap switch to RFRs . Those those changes of market behavior is a further prove that the ISDA-designed fallback is not fit for p...